Brand Experience (BX) Expert is a feature series initiated by Novaon Digital in collaboration with industry experts to provide in-depth, practical analysis on brand-building strategies. Each article uncovers key trends, insights, and lessons to help businesses adapt and create lasting value.

Q: Hello Ms. Vy. From your perspective, what are the defining psychological and financial behaviors of Gen Alpha and Gen Z in the 2025+ landscape? How do they differ from Millennials in terms of engaging with financial products and brands?

Gen Alpha and Gen Z exhibit distinctive patterns in how they approach financial matters – sharply diverging from their Millennial predecessors. This is precisely why, in the coming years, I anticipate a fundamental shift in how banks communicate and deliver their services.

Several key trends are emerging among these two generations:

Firstly, Gen Alpha has grown up in a world where waiting is virtually obsolete. Raised in an environment powered by AI-generated instant content and on-demand services—spanning education to finance – they expect immediacy. Banks can no longer expect them to queue or wait days for approval; services must be instant.

Gen Alpha’s financial behavior

This generation gravitates toward engaging, interactive, and trend-driven experiences. Many financial platforms are responding by incorporating gamification elements and deploying AI as virtual advisors – turning financial transactions into game-like, enjoyable experiences that are both efficient and fun.

Gen Z’s financial behavior

Gen Z, on the other hand, demonstrates financial literacy and investment awareness much earlier than Millennials. They understand the value of money, yet they reject long-term commitments to financial institutions. Unlike older generations who remain loyal to banks out of habit, Gen Z chooses platforms that are flexible, convenient, and aligned with their lifestyle. This explains the rapid rise of fintech, e-wallets, and digital banking.

While Millennials may see banks as vehicles for saving and wealth-building, Gen Alpha and Gen Z view finance as a tool for enhancing life experiences. They are impatient with bureaucratic procedures and less loyal to any one brand. What they seek are brands that truly meet their personal needs – and they’re not hesitant to switch if those needs evolve.

Q: In 2025, the banking sector is undergoing a major digital transformation with AI, hyper-personalization, and decentralized finance (DeFi). How are these technologies changing the way Gen Alpha and Gen Z interact with financial services?

By 2025, we’re witnessing more than a digital transformation – it’s a redefinition of how financial services operate. I’ve observed three key technological forces reshaping the industry, and banks must take heed to avoid being left behind.

First, AI has evolved beyond a support tool into a true “personal financial assistant.” Where AI once powered chatbots and data analytics, by 2025, it is expected to learn individual spending habits, predict financial needs, and proactively offer solutions—sometimes before users even realize they need them. This has sparked a tech race, pressing banks to either lead in AI innovation or invest heavily to stay competitive.

Simultaneously, Web3 and DeFi are reshaping young generations’ perceptions of the financial system. Gen Z is already leaning toward more flexible alternatives beyond traditional banks, while Gen Alpha is growing up in a world where blockchain, stablecoins, and peer-to-peer financial models are increasingly normalized and accessible. They no longer rely solely on banks for loans or investments—they’re engaging directly on decentralized platforms.

Another crucial trend is the rise of financial super apps. Today’s youth don’t want multiple apps for money management—they want a single, all-in-one platform for payments, investments, insurance, and passive income.

Technology’s Development has impact on Gen Z and Gen Alpha financial behavior

I believe that from 2025 onward, finance is no longer the exclusive domain of banks. Without adapting, banks risk losing Gen Alpha and Gen Z to faster, more flexible, and more personalized financial alternatives. This isn’t just a tech upgrade—it’s a systemic transformation in how banks operate, communicate, and create real value for the next generation.

Q: What are the biggest challenges banks face in building strong connections with these younger generations? Could you share some key reasons behind these difficulties?

There are three main challenges that I see banks grappling with when engaging Gen Alpha and Gen Z.

First is the shift in how trust and brand experience are built. In the past, legacy reputation alone was enough. Now, trust stems from real experiences. These generations engage with brands digitally, via community content and social media—not through corporate declarations. Security and reliability remain vital, but they must be communicated in a language and medium these generations relate to. The way forward is for banks to listen more, experiment boldly, and stay culturally relevant.

Brand Experience is key element for Gen Z and Gen Alpha

Second is the challenge of innovation speed. Banks, burdened by complex systems and regulatory compliance, struggle to match the agility of fintechs. Meanwhile, Gen Alpha and Gen Z expect seamless, rapid experiences and will swiftly switch to more efficient services if faced with delays.

Lastly, personalization is no longer optional – it’s expected. These generations reject being lumped into generalized customer segments. They want services tailored to their behavior, preferences, and financial goals. Achieving large-scale personalization demands robust data capabilities, powerful AI, and a flexible mindset in product development—something many traditional banks are still building toward.

Q: Many international banks are adopting creative communication models like “Banking as a Lifestyle” to appeal to younger generations. Could you share a successful case study from Vietnam or abroad?

“Banking as a Lifestyle” is more than a communication model – it’s a business and customer experience strategy. This approach repositions banks from traditional service providers to lifestyle platforms embedded into daily living. Rather than just storing money or facilitating transactions, banks become ecosystems that connect essential needs—shopping, travel, entertainment, investing, and financial wellness.

Technology is the linchpin, enabling personalized, fast, and convenient experiences that resonate with Gen Z and Gen Alpha – who value connectivity and attractive incentives. This shift transforms not just communication but the entire structure of financial products, services, and partnerships.

One standout example in Vietnam is Cake by VPBank. This digital bank – born from a partnership between VPBank and Be Group – offers more than just financial services. Fully integrated into the Be app, users can open accounts, make payments, and access lifestyle perks without leaving the ecosystem. Lifetime free transactions further encourage young customers to adopt and stay engaged.

A success case study in “Banking as a Lifestyle”

Cake’s branding is equally disruptive – its name, logo, and vibrant pink color scheme set it apart in a market dominated by blue and red tones. The name “Cake” conveys simplicity and ease – finance made “as easy as eating cake.” This clever positioning makes banking feel accessible and fun for younger users.

Ultimately, “Banking as a Lifestyle” is not just a communications campaign. It’s a strategic direction requiring banks to redesign products, apply new technologies, and cultivate partner ecosystems to deliver meaningful value.

Q: If you had to offer just three key pieces of advice to banks aiming to optimize their communication strategy for Gen Alpha and Gen Z in 2025, what would they be?

In my view, brand experience is the decisive factor when it comes to connecting with Gen Alpha and Gen Z. These generations evaluate banks not just on products, but on how brands appear and interact with them. If the experience isn’t seamless or doesn’t match their digital behavior, they’ll quickly move on.

Momo’s Brand Experience strategy and youth engagement

To succeed, banks must embed themselves into the ecosystems these generations already use. Gen Z doesn’t want to download another app. Gen Alpha is even less invested in “choosing” a bank. Financial services must be integrated into their existing platforms—from social media to e-commerce.

Personalization is another cornerstone. It’s more than inserting a name into an email—it’s about delivering the right content, at the right time, in the right context. If the message doesn’t match their actual needs, the brand experience will feel distant and irrelevant.

Finally, banks must go beyond product-centric messaging and focus on value creation. Gen Z and Gen Alpha want brands that empower them to manage finances better or contribute meaningfully to their communities. If a brand lacks emotional or social resonance, it will struggle to retain these customers.

Q: Looking ahead, what is your forecast for the future of financial and banking communications over the next five years, as Gen Alpha and Gen Z become the dominant customer segments?

In the next five years, brand communication in the financial and banking sector must undergo a profound redefinition to align with how Gen Alpha and Gen Z perceive value. These generations aren’t just looking for strong financial products – they want immersive brand experiences, personalized interactions, and evidence of a brand’s social impact.

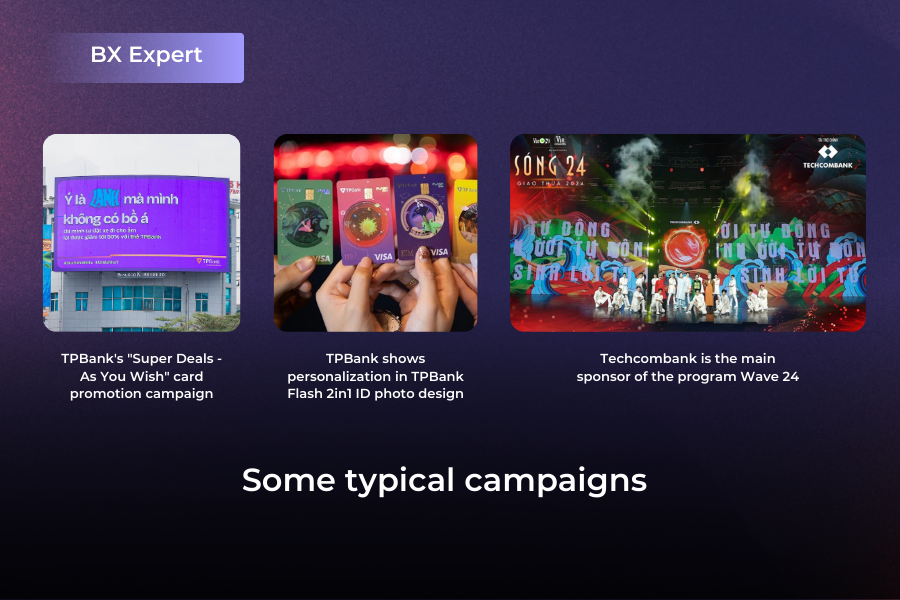

Some typical campaigns to reach young people through brand experience, personalization and social role of banks

From my perspective, banking brands can no longer rely solely on stability and legacy reputation. Today, what defines a strong brand is its ability to deliver intuitive, accessible, and meaningful financial experiences tailored to each individual.

This transformation isn’t a passing trend – it’s a structural shift. Banks that embrace real-world experience design and adapt their brand strategies accordingly will be well-positioned to win the hearts and wallets of tomorrow’s customers.

Thank you, Ms. Vy, for this insightful discussion!

Source: Brandsvietnam